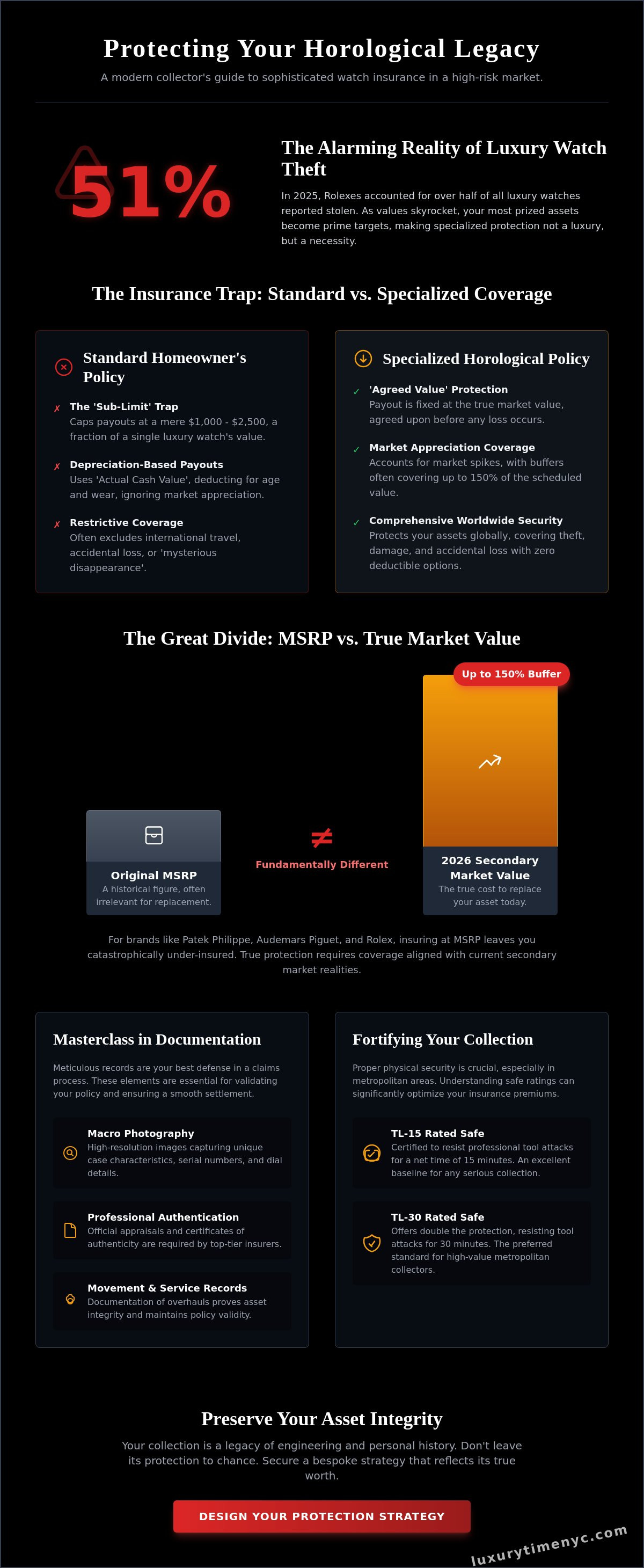

In 2025, Rolex accounted for 51% of all luxury watches reported stolen, a stark reminder that your most prized assets are also the most targeted. For the discerning collector, this reality is compounded by a market where values often outpace coverage limits. You've curated your pieces with precision, yet the rapid market shifts of 2026 mean that insuring a luxury watch collection has become a complex endeavor. Standard policies often fail to account for the three global price increases Rolex implemented in the last twelve months alone.

You likely recognize that your collection represents more than just financial value. It's a legacy of fine engineering and personal history. Discover how to protect your horological investments with a sophisticated approach to valuation, specialized coverage, and strategic documentation. This guide explores the transition from basic insurance to a bespoke strategy. We cover everything from navigating metropolitan theft risks to securing agreed-value terms that reflect the true rarity of your mechanical assets.

Key Takeaways

- Avoid the 'sub-limit' trap found in standard residential policies by securing specialized, standalone protection for your horological assets.

- Align your coverage with 2026 secondary market values rather than original MSRP to ensure complete replacement capability for brands like Patek Philippe and Audemars Piguet.

- Master the strategic approach to insuring a luxury watch collection through high-resolution macro photography and meticulous documentation of unique case characteristics.

- Optimize your insurance premiums by understanding the technical nuances of TL-15 and TL-30 safe ratings for metropolitan residences.

- Learn why professional authentication and movement overhauls are essential requirements for maintaining the validity of top-tier insurance contracts.

Why Standard Homeowners Policies Fail Luxury Watch Collectors

Standard homeowners insurance is designed for the predictable. It protects residential structures and common household goods. For the serious collector, relying on these generic contracts is a profound risk. Most residential policies contain a 'sub-limit' trap. This clause often caps the payout for jewelry and timepieces at a mere $1,000 to $2,500 per item. When insuring a luxury watch collection, such limits are catastrophically insufficient. A single Patek Philippe or Audemars Piguet requires protection that respects its market gravity.

Standard policies often fall short in three critical areas:

- Restrictive sub-limits that cap payouts at a fraction of a watch's value.

- Settlement structures based on depreciation rather than market appreciation.

- Exclusions for common scenarios like accidental loss or international travel.

Generalist adjusters typically rely on standard insurance principles that prioritize depreciation. They view a watch through the same lens as a television or a sofa. This approach is fundamentally flawed. While common assets lose value, rare timepieces often appreciate. Standard policies frequently utilize 'Actual Cash Value' settlements. These settlements deduct for age and wear, ignoring the reality of the 2026 secondary market where rarity commands a premium.

Geographic limitations also pose a threat. Standard policies often include restrictive clauses regarding location. They frequently exclude 'mysterious disappearance,' which refers to items lost without a witnessed theft. For a traveling connoisseur, this exclusion is a significant vulnerability. Specialized insurance provides worldwide coverage. It ensures your investment is secure whether it rests in a Manhattan vault or accompanies you to a private viewing in London. True security requires a policy that travels as well as you do.

The Limitations of Generalist Underwriters

Generalist underwriters lack the technical vocabulary of fine horology. They cannot distinguish between a standard dial and a rare 'Tiffany-stamped' variant. To them, a reference number is a mere string of digits. This lack of expertise leads to inadequate coverage. Depreciation scales in standard policies are incompatible with appreciating assets like a vintage Rolex. You risk a settlement that fails to cover the cost of a comparable replacement in today's surging market.

Specialized Horological Coverage: A Peerless Alternative

Specialized insurance is the only logical choice for insuring a luxury watch collection. These policies offer 'Agreed Value' terms. You and the insurer establish a fixed payout amount before any loss occurs. This honors the collector's knowledge and the piece's provenance. Many elite policies offer zero-deductible options for high-net-worth individuals. They also cover partial damage. This includes the high cost of professional restoration required to maintain the integrity of a complex movement.

Calculating the Real Value: Market Price vs. Original MSRP

Valuation is the cornerstone of any strategy for insuring a luxury watch collection. In 2026, the delta between a manufacturer's suggested retail price (MSRP) and actual market value has reached unprecedented levels. For brands like Patek Philippe and Audemars Piguet, the retail price is often a fiction. It bears little resemblance to the capital required to replace a lost asset on the secondary market. If your policy is pegged to the original receipt, you are profoundly under-insured. True protection requires a replacement cost tied to immediate secondary market availability.

Elite insurers now offer a Market Appreciation Buffer. This provision allows for a payout above the scheduled value, often up to 150 percent, to account for sudden market spikes. Standard Inflation Guard clauses are typically fixed at modest percentages. They are designed for traditional household goods. They fail to keep pace with a rare timepiece that might appreciate twenty percent in a single quarter. For the serious collector, these generic adjustments are insufficient. You require a policy that understands the velocity of the 2026 horological market.

The Volatility of Investment-Grade Timepieces

Market movements are swift and often permanent. Consider the Rolex nyc landscape. A stainless steel professional model can double in value within months of a discontinuation announcement. In 2026, collectors must treat their portfolios as living entities. Annual re-evaluations of agreed value are no longer optional. They are a necessity for maintaining asset integrity. If you haven't updated your appraisals since the sweeping Rolex global price increases on January 1st, 2026, your coverage is likely obsolete. It is prudent to seek professional authentication services to establish a current, undeniable baseline for your inventory.

Scheduled Items vs. Blanket Coverage

Precision requires categorization. Scheduled Personal Property is the gold standard for insuring a luxury watch collection. Each piece is individually listed with its own agreed value and technical description. This ensures total clarity during a claim process. Conversely, blanket coverage provides a lump sum for a group of items. It is often suitable for lower-value accessories. Many connoisseurs adopt a hybrid approach. They schedule their icons, such as a Richard Mille or a Royal Oak, while blanketing their entry-level luxury watches that fall within the $4,000 to $7,000 range. This strategic layering optimizes both protection and premium costs.

The Essential Documentation Masterclass for Claims Success

Documentation is the ultimate safeguard. It transforms a tragic loss into a seamless recovery. For those insuring a luxury watch collection, a definitive archive is non-negotiable. It's the language underwriters speak. You must move beyond the casual records of the past. A simple snapshot is insufficient. A professional archive requires depth. Accuracy. Absolute transparency.

Every new acquisition demands a rigorous intake process. This checklist ensures your claim remains indisputable:

- Macro Imagery. High-resolution photography of the movement, serial numbers, and unique case markings.

- Physical Provenance. Scanned copies of original sales receipts and warranty cards.

- Current Appraisals. Documents reflecting the 2026 market value, not the purchase price.

- Service History. Records of movement overhauls or pressure testing to prove 'working order'.

High-resolution macro photography is essential. It identifies unique case characteristics that serial numbers alone might miss. Tiny marks. Specific graining on the lugs. These are the fingerprints of your timepiece. Store original physical documents in a secure, off-site location. A bank vault is ideal. For the digital age, maintain a 'Digital Vault'. This encrypted repository should be easily accessible to your adjuster. It provides the transparency required for a rapid, undisputed settlement.

Professional Appraisals: The Gold Standard

An invoice is a moment in time. An appraisal is a professional judgment of value. In the luxury sector, insurers require USPAP-compliant appraisals. These are formal documents that stand up to legal scrutiny. For a Patek Philippe New York collection, you must refresh these valuations every 12 to 18 months. The 2026 market is too volatile for outdated data. An appraisal from 2024 is a liability, not a protection.

Chain of Custody and Provenance

Provenance is the soul of value. Service records prove the watch was maintained with care. They verify the movement remains within manufacturer specifications. Originality is the primary driver of market premium. You must document any replaced parts or service dials. Use watch repair nyc records as definitive proof of condition. This chain of custody preserves asset integrity. It ensures your insurer respects the rarity and technical health of every piece in your portfolio.

Security Strategies for the Modern Metropolitan Collector

Security is a philosophy of protection. It extends beyond the physical vault into the daily habits of the connoisseur. When insuring a luxury watch collection, the premium you pay is often a reflection of your security protocols. Insurers utilize distinct 'In-Vault' and 'In-Wear' premium structures. Keeping a rare Patek Philippe in a bank vault or a certified home safe significantly reduces the annual cost. However, the true purpose of a collection is the pleasure of the wear. Balancing these costs requires a strategic approach to risk management.

Home safe technology has evolved to meet metropolitan threats. For Manhattan residences, insurers often mandate TL-15 or TL-30 rated safes. These ratings signify that the safe can resist professional tool attacks for 15 or 30 minutes, respectively. A standard fire safe is insufficient for high-value horology. You require a burglary-rated sanctuary. When traveling, use a discreet, multi-watch roll. Never leave it in a hotel safe. These are notoriously vulnerable. Keep your pieces on your person or in a bonded vault.

The goal of robust insurance is to remove the psychological barrier of ownership. You shouldn't be afraid to wear your investment. A sophisticated policy provides the freedom to enjoy a Richard Mille in public, knowing that the financial value is absolute and protected. If you are unsure of your collection's current security standing, a professional watch authentication and consultation can establish the baseline for your insurance requirements.

NYC-Specific Risk Mitigation

The 47th Street New York watches scene remains a global hub, yet it demands high-level awareness. Secure transport between dealers and your residence is paramount. Insurers often require specific protocols for Manhattan residents, such as using armored couriers for high-value acquisitions. Choose your daily wear with discretion. A subtle Cartier may be more appropriate for a metropolitan commute than a high-complication piece intended for a private event.

The Claims Process: What Happens After a Loss

Immediate action is critical following a loss in NYC. You must file a police report within 24 hours. Specialized insurers do not just offer a check. They utilize global networks to source exact replacements for rare models. This is vital for discontinued references that are no longer at retail. You often have a 'Cash Out' option, providing the full agreed value, or a 'Replacement' option where the insurer handles the procurement. This bespoke service ensures your collection's narrative remains intact even after a theft.

Preserving Asset Integrity with Luxury Time NYC

Asset integrity is the silent partner of a robust insurance policy. When insuring a luxury watch collection, the validity of your coverage rests upon the verifiable health of your timepieces. Insurers don't merely protect a brand name; they protect a functioning, authentic mechanical asset. Neglecting professional maintenance can jeopardize a claim. A movement that hasn't seen a professional movement overhaul in a decade may be viewed as a liability rather than a treasure. Luxury Time NYC serves as the guardian of this integrity, providing the meticulous authentication that elite underwriters demand.

The relationship between movement health and 'functional value' is absolute. A watch that fails to keep time or lacks water resistance—verified through regular pressure testing—may be appraised at a lower tier. This affects your 'Agreed Value' and your eventual payout. Maintaining your collection isn't just about aesthetics. It's about preserving the investment grade of the piece. Expert sourcing also plays a vital role in the recovery phase. Should a loss occur, specialized adjusters often turn to trusted metropolitan institutions to source certified authentic replacements for rare, discontinued models.

Expert Authentication and Valuation Services

Our expertise provides the definitive documentation required for high-complication pieces. Whether it's a Richard Mille or a vintage Patek Philippe, we establish the baseline of truth. This includes:

- Watch Authentication. Absolute verification of every component, from the hairspring to the dial.

- Valuation. Market-current appraisals that reflect the 2026 secondary market surges.

- Condition Reports. Detailed accounts of movement health and case originalness.

A professional movement overhaul is essential for maintaining investment grade. It ensures the 'functional value' remains peak. We act as a preferred partner for global insurance adjusters, providing the technical clarity they lack. This bridge between the collector and the insurer is what secures your legacy.

The Luxury Time NYC Advantage

Since 2005, we've maintained a tradition of excellence in the heart of the New York Diamond District. Our institution is built on quiet confidence and deep industry knowledge. We offer comprehensive horological support, from the initial acquisition of a Rolex or Cartier to professional repair and polishing. We don't just sell timepieces; we curate and protect fine mechanical arts. When insuring a luxury watch collection, your choice of advisor is as important as your choice of insurer. Protect your legacy—consult Luxury Time NYC for your next valuation.

Securing the Future of Your Horological Legacy

The 2026 market demands a departure from traditional insurance models. Protecting your assets requires more than a standard policy; it necessitates a commitment to market-current valuation and rigorous documentation. You've moved beyond the limitations of residential coverage to embrace a strategy that respects the rarity of your portfolio. By prioritizing agreed-value terms and certified security protocols, you ensure that your investment remains a source of pride rather than a point of vulnerability.

A sophisticated approach to insuring a luxury watch collection is anchored in professional expertise. Success in the event of a loss is determined by the quality of your provenance and the health of your movements. Every service record and high-resolution photograph serves as a testament to the authenticity and value of your collection. This meticulous attention to detail is what defines a true connoisseur.

As a Diamond District institution since 2005, we offer the specialized authentication and valuation required by top-tier insurers. Our expertise in Rolex, Patek Philippe, and Audemars Piguet ensures your documentation is indisputable. Secure Your Collection with a Professional Valuation at Luxury Time NYC. Your legacy deserves the protection of absolute certainty.

Frequently Asked Questions

Is my luxury watch collection covered by my homeowners insurance?

Standard homeowners policies are generally insufficient for horological assets. Most contain a sub-limit clause that caps jewelry coverage at a nominal amount, often between $1,000 and $2,500. For those insuring a luxury watch collection, this creates a significant coverage gap. You require a standalone policy or a specific rider that schedules each piece at its full market value. This ensures your protection isn't tethered to the restrictive limits of a residential contract.

How often should I have my watch collection appraised for insurance?

You should refresh your appraisals every 12 to 18 months. The 2026 market moves with a velocity that renders older documents obsolete. With global price increases occurring multiple times a year, a static valuation is a risk. Regular updates ensure your coverage reflects the current capital required for a replacement. It's a necessary discipline for maintaining the integrity of your financial protection and ensuring you aren't under-insured during a market surge.

What is 'Agreed Value' and why is it better for luxury watches?

Agreed Value is a predetermined settlement amount that doesn't account for depreciation. It's the gold standard for insuring a luxury watch collection because it honors the asset's appreciation. Unlike Actual Cash Value, which deducts for wear and age, Agreed Value guarantees a specific payout established at the policy's inception. This provides absolute certainty and eliminates the friction often found during the claims process with generalist insurers who don't understand horological rarity.

Does watch insurance cover damage or just theft and loss?

Specialized policies extend far beyond theft and total loss. They typically cover accidental damage, such as a cracked sapphire crystal or a compromised movement. This includes the high cost of professional restoration required to maintain the piece's provenance. Standard policies often exclude these partial losses, leaving the collector to fund expensive repairs out of pocket. A bespoke policy treats damage as a protected event, ensuring the mechanical integrity of your investment remains intact.

Will my insurance premium go down if I keep my watches in a bank vault?

Yes, premiums for items stored in a bank vault are often significantly lower than those for daily wear. Insurers categorize these as In-Vault risks, which carry a much lower probability of theft or accidental damage. If you choose to wear a vaulted piece for an event, you must notify your insurer to activate temporary In-Wear coverage. This strategic layering allows you to protect a large portfolio without incurring excessive annual costs.

What documentation do I need to file a successful watch insurance claim?

Success depends on a tripartite archive of evidence. You need a USPAP-compliant appraisal, high-resolution macro imagery, and proof of purchase or authentication. These records should be stored in an encrypted digital vault accessible to your adjuster. In 2026, insurers expect a transparent chain of custody. Providing meticulous documentation of service history and unique case markings ensures your claim is processed with the speed and respect your collection deserves.

For those who also collect high-end gold and diamond pieces, it is worth your time to check out BOS Jewelers Inc, a family-owned institution with over 40 years of experience in providing quality jewelry and expert service.

Does insurance cover the loss of value if a watch is repaired with non-original parts?

Most standard policies don't cover the diminution in value that occurs when a watch is repaired with non-original parts. They only cover the functional repair cost. For high-complication pieces, the loss of a period-correct dial can erase a significant portion of market value. You must ensure your policy includes a clause that mandates repairs use only manufacturer-certified components. This preserves the asset's investment grade and historical authenticity over the long term.

Can I insure a watch I bought on the pre-owned market without original papers?

Yes, you can insure a watch without original papers, provided you have a professional authentication. An expert appraisal from a recognized metropolitan institution replaces the need for original warranty cards. It establishes the piece's legitimacy for the underwriter by verifying serial numbers and movement caliber. While original box and papers enhance market desirability, a certified appraisal is the only document required to establish an insurable interest and an agreed value for your policy.